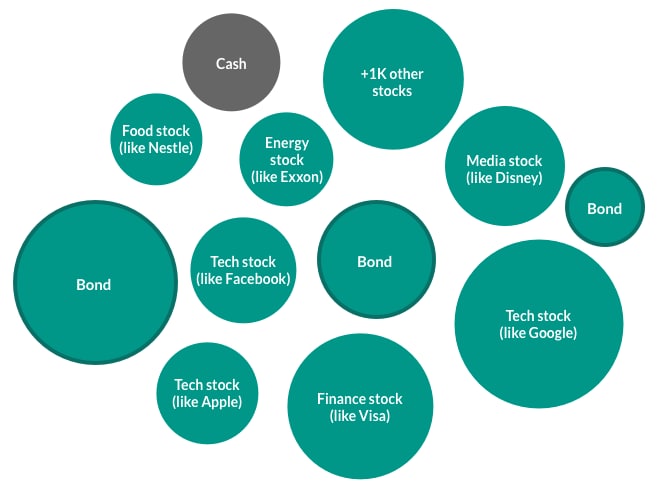

The anatomy of an ETF.

We broke down the inside of an ETF to give you a better idea

of what a potential investment could look like.

The companies we show are used as examples and aren’t meant to

represent a particular or actual ETF.

The cost of ETF investing

ETFs are typically passively managed (compared to actively managed mutual

funds).

This means that instead of a fund manager using their knowledge to select the

investments in the ETF, they simply select securities to try and keep pace with

a major

benchmark, like the Dow Jones Industrial Average or the Russell 2000

Since they’re less time-intensive for brokerages, ETFs tend to have lower

expense ratios (a.k.a.

the cost for operating and managing a fund) than many other investment choices.

Even better, when you invest in ETFs, you’re able to invest in hundreds or even

thousands

of securities with just one transaction. Not only does this allow ETF investors

to hold portions

of stocks they might not be able to afford otherwise (like Berkshire Hathaway),

but it can also mean

commission-free trading.

Before you invest, you should carefully review and consider the investment

objections, risks, charges and

expenses of any ETF you are considering. ETF trading prices may not necessarily

reflect the net asset

value of the underlying securities.